A central issue of contestation is elasticity versus discipline, elasticity for me and discipline for you, alchemy of banking and money funding for me, austerity and borrowing/payment for you.

Perry Mehrling, Liquidity Changes Everything

Like 2009, the (coming/arriving) financial collapse of 2020 will reveal the asymmetry of power between the financial sector and the rest of the economy, and it’ll especially highlight how the financial sector is continually privatizing profits and socializing losses.

When you see terms in the media about the Fed “expanding its balance sheet” think: “The Fed is literally buying failed financial instruments to prevent banks and financial companies from going out of business”. Currently, according to Section 14 of the Federal Reserve Act, the Fed is prevented from buying assets (stocks, index funds CDO: Collateralized Debt ObligationCDO, mortgage backed security directly on the market. Instead they can only buy government-backed assets, mostly bonds and MBSs by institutions like Freddie Mac that are government backed. Instead, the Feds first line of defense is lowering interest rates, and then creating liquidity by buying long-term maturities.

With the interest rates at zero, the biggest lever at the Fed is effectively broken, and now they’ve got to find another lever. March 6th, 2021Last Friday, Boston Fed President Eric Rosengren called on Congress to expand the Fed’s powers to buy and sell a broader range of assets. This will require congressional approval, and during this period of crisis, I’m certain Shock Doctrine politics will win out, and these ammendments will pass. I hope I’m wrong.

So what does this mean? This means that the Fed can start buying non-government

backed securities: potentially any failing public stocks, private CDOs and

MBSs1. What this means is

the Fed can buy the most dangerous, volatile, and toxic assets that nobody else

is buying, the ones that are the first to fail in a bursting bubble. This is a

Fed that has institutionalized & encouraged systemic moral hazard—saying,

in effect: If you (the finance sector) create risky assets and they

fail, we’ll allow you to profit during the good times and we’ll save you by

buying them back during the bad times

.

Remember the Nobody remembers the Zune, it failed horribly.Microsoft Zune mp3 player? Now imagine Microsoft had put so much investment into its Zune, that when nobody bought it, and the product failed, the company would’ve gone bankrupt. Now, if this were the financial sector, this is where the Fed becomes the Dealer of Last Resort, steps in and buys all the Zune mp3 players, saving Microsoft from going bankrupt.

This is exactly what the Fed is doing when it says it is “expanding its balance sheet”—its buying the failed assets the financial industry has created over the last 10 years, those very same assets the industry has made huge profits from; but now that the profits have stopped, the Fed bails them out by buying them when no one else will.

Update: January 2021Nearly 10 months2 since this essay was published, we’re already seeing strong indicators that consumer purchasing power will be severely hurt by inflation. So while government stipends may help in the near short term, long term people will be hurt by less value for every dollar they earn.

When the Fed goes to congress to ask for changes to Section 14, they will use

the Shock Doctrine playbook: the banks will fail

, retirement funds

will tank

, companies will go out of business

, we’re in desperate

times, so we need to take desparate measures

. These predictions are all

true, and these outcomes will happen: but the solution they offer only addresses

the symptoms, but not the root cause—the

deregulation of the

financial sector. Neoliberal deregulation of the financial sector over the last

40 years has encouraged banks to put money into risky bubbles that keep popping,

retirement funds of regular people are directly tied into that system, even

fueling it. This is wrong. I’m not generally opposed to these risky

investments, but these investments must be separated from investment banks,

and kept out of any fund designed for peoples retirements and long term savings.

These asset types need to be drastically limited to qualified investors and

speculators only.

As it stands, bailouts will reward the most risky investors and speculators, while passive investors, retirees, and taxpayers will end up bailing out these risk takers. We’ve already seen it happen, specifically, the gutting of the Volcker Rule, the repeal of the affiliation restrictions of the Glass–Steagall Act, and the giant free-for-all stock buybacks taking place.

The only ways to mitigate risk-loading is strict limitations on executive compensation, employee bonuses, and no mergers or acquisitions for at least 10 years. These banks should be nationalized, its execs fired and all contracts voided. New leadershp will be brought in as reasonably paid public servants.

Thus, for the finance sector, the Fed provides elasticity: fungible rules around banking, investing, taxation, and bailouts when things go bad. For the rest of the economy, and individuals, we get discipline: massive losses, austerity and cuts to social programs and public infrastructure, moralizing our individual failures as people, capitalizing on the large-scale failures of small businesses3, and continual indebtedness for the poor and middle classes.

This is an ideological conservatism combined with a blind faith in an economics

that can never be wrong. As Frank Wilhoit put it Conservatism consists of

exactly one proposition, to wit: There must be in-groups whom the law protects

but does not bind, alongside out-groups whom the law binds but does not

protect

(See

The travesty of liberalism

by Frank Wilhoit 2018). Only the in-group is an

autonomous, rogue financial sector, and the politial interest groups they fund.

The out-group is everyone else.

In this way the finance industry can reap the profits of risky financial instruments, but when the risk generates market failures, the Fed bails them out. It’s all upside, and no downside. This is the very definition of moral hazard. The financial industry literally cannot lose because the Fed will always save them.

In effect, this is Socialism for the rich, rugged individualism for the

poor

—Martin Luther King, Jr. (pp 346).

Lemon socialism is a pejorative term for a form of government intervention in which government subsidies go to weak or failing firms (lemons; see Lemon law), with the effective result that the government (and thus the taxpayer) absorbs part or all of the recipient’s losses. The term derives from the conception that in socialism the government may nationalize a company’s profits while leaving the company to pay its own losses, while in lemon socialism the company is allowed to keep its profits but its losses are shifted to the taxpayer.

Lemon Socialism Wikipedia

So the imbalance: Why does the Fed continually save the financial industry every 10 years, but not any other industry? Why does the Fed create and spend 1.5T dollars to purchase worthless and arcane financial instruments, but never spend on public goods like housing, student education, public infrastructure?

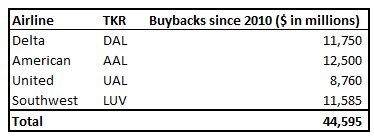

This is our biggest opportunity, while we have the most leverage, to heavily invest in public infrastructure and works programs. The airline industry is already asking for bailouts to the tune of $50B. This isn’t the time for bailouts, this is the time for imagination, to create a society that works for everyone. This is the time to nationalize the airline industry. Since 2010, the very same industry has been investing their money directly into stock buybacks, pumping up their own stock prices, and paying huge bonuses to their execs and CEOs. Since 2010 the major airlines have invested $45B in buybacks, and now asks for $50B in bailouts.

This means that they spent $45B of their own money betting that their stocks would go up in value, paying out any profits to their execs and CEOs as their valuations rose, and when the market burst, they asked for their money back and an additional $5B on top. To put this simply, this is a massive con-job and outright theft. Nationalizing the airline industry is a win-win: it will create good paying american jobs, make flying more affordable, mitigate cost cutting at the expense of flight safety (see ‘Boeing 737 Max’), and mitigate market risk.

And now we get to the systemic asymetries of power. Trump and those within his

inner circle, as well as his political base believe they are entitled to the

rights and protections of the law, and meanwhile cast blame and stigmatize those

least able to defend themselves. Their in-group will be the first to receive the

benefit of any bailouts, and the negative consequences will be blamed upon, and

most adversely affect the out-group. As

Adam Serwer

puts it: the cruelty is the point

:

Only the president and his allies, his supporters, and their anointed are entitled to the rights and protections of the law, and if necessary, immunity from it. The rest of us are entitled only to cruelty, by their whim. This is how the powerful have ever kept the powerless divided and in their place, and enriched themselves in the process.

Adam Serwer, The Cruelty is the Point

We, as a society are starting to understand that the financial sector is rotten to the core, and this rot is going to seep into public sentiment: “If they don’t play by the rules, why should I?“. This has the effect or eroding the very conception of a nation operating under an equal rule of law, and will result in toxic resentment and fuel civil unrest.

Footnotes

-

Update: April 9th, 2021

As predicted, the Fed is starting to take consumer credit debt and commercial MBSes onto its balance sheet.The Fed will now accept triple-A rated tranches of existing commercial mortgage-backed securities and newly issued collateralized loan obligations. Under TALF, the Fed lends money to investors to buy securities backed by credit-card loans and other consumer debt. The Fed has made $100 billion available for that program and didn’t increase the amount Thursday.

Fed Expands Corporate-Debt Backstops, Unveils New Programs to Aid States, Cities and Small Businesses ↩ -

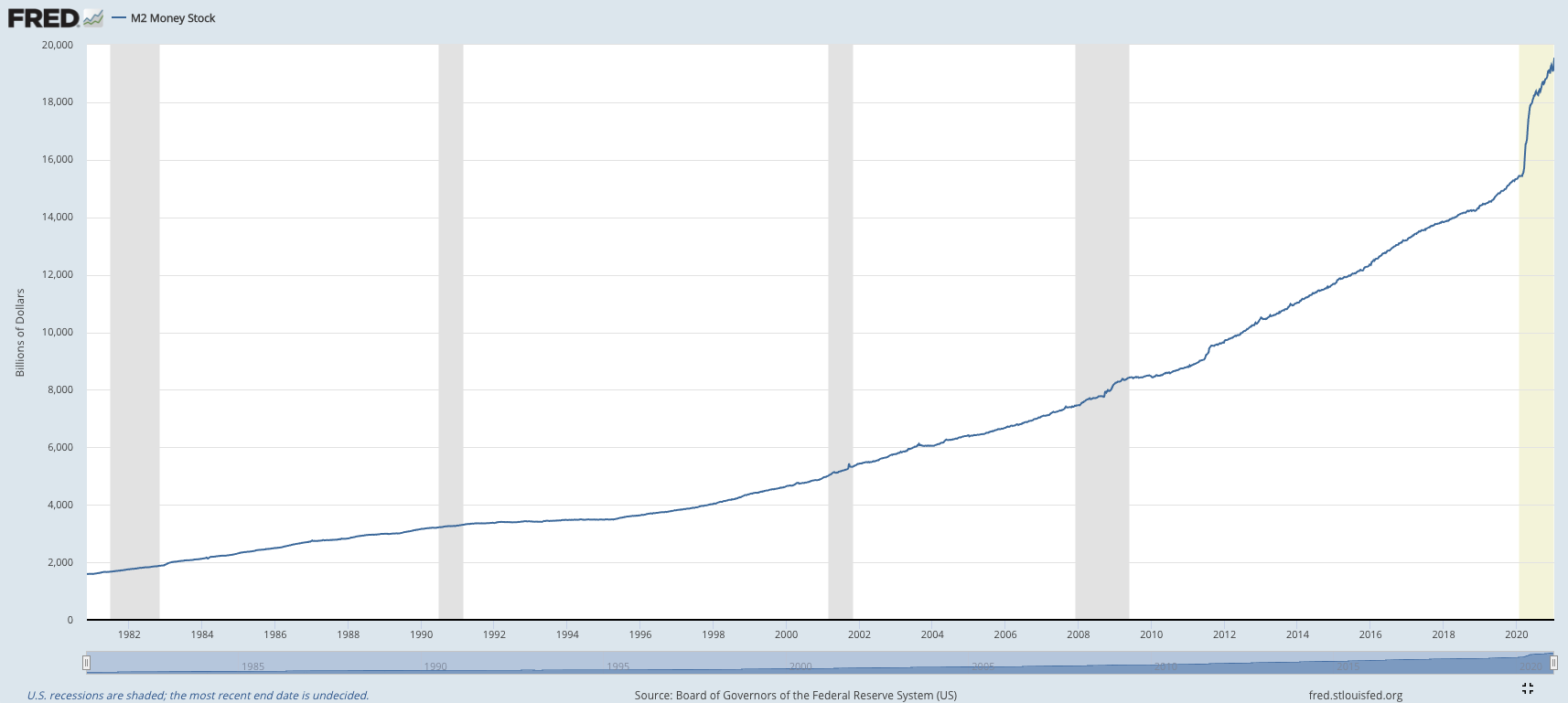

Update: January 25, 2021

Added a chart of the FRED M2 Money Stock from the Federal Reserve Bank of St. Louis.

M2 is closely watched as an indicator of money supply and future inflation, and as a target of central bank monetary policy. M2 is a calculation of the money supply that includes all elements of M1 as well as “near money.” M1 includes cash and checking deposits, while near money refers to savings deposits, money market securities, mutual funds, and other time deposits. These assets are less liquid than M1 and not as suitable as exchange mediums, but they can be quickly converted into cash or checking deposits. ↩ -

Update: March 25th, 2021

After reviewing early drafts of the Take Responsibility for Workers and Families Act, as proposed, Wall Street, will suddenly have $4-6T of government guaranteed low cost credit to go shopping for businesses in trouble. We would see the mother of all roll-ups, as small and medium sized businesses desperately try to get whatever they can from deep-pocketed private equity investors and monopolists. If that happens, the America we know, of heterogeneous small businesses would look very different after this pandemic is over—a homogeneous space optimized for massive corporations and destroying local autonomy and diversity. ↩